May 12, 2022

Loan Officer, Mortgage InsuranceUnderstanding the Next Generation of Homebuyers - The ABCs of Gen Y and Z

A New Home Buyer Demographic Is Emerging.

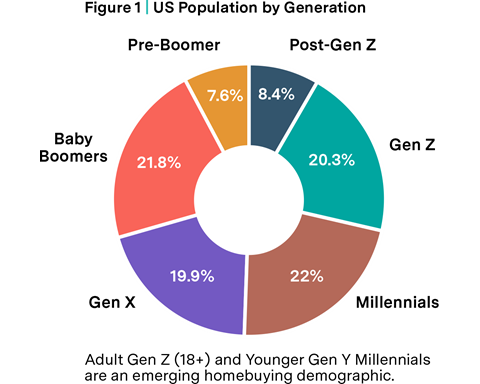

The homebuyer market is always changing but will see some dramatic shifts in the next few years as Younger Gen Y Millennials and members of Generation Z become an increasing share of the home-buying public. These younger generations make up more than 20% of today’s population and are poised to overtake older cohorts in number of homes purchased.1

In June 2021 surveys, 21 percent of Generation Z adults said they were planning to buy a home in the next 12 months, 43% said they expect to buy a house within five years and 45% said they are already saving for one.2,3 Younger Gen Y Millennials, those born from 1990 to 1998, are already making their mark on the housing industry. This cohort bought 14% of homes sold from mid-2019 to mid-2020, a year-over-year increase of 27% and the most substantial gain of any generational cohort.4

Understanding the characteristics, behaviors, and buying trends of Gen Z and Younger Gen Y Millennials can help loan originators make informed decisions about how to reach and work with the next generations of home buyers.

In part one of our three-part series, Understanding the Next Generation of Homebuyers | The ABCs of Gen Y and Z, we look at the demographics and sociographics that distinguish younger members of Generation Y and define rising members of Generation Z.

|

|

Demographic and Sociographic Differences

The Gen Y Divide.

Perhaps no other demographic has been analyzed and reported on more than the Millennial Generation, those late bloomers who eschew traditional career paths, prefer experiences to “things,” and delay the milestones that impact household formation (moving out, getting married, and having children). Less has been reported on the generational divide between younger and older members of this cohort.

Sociologists (and marketers) now recognize that there are differences worth noting when working with younger versus older members of the Millennial Generation.

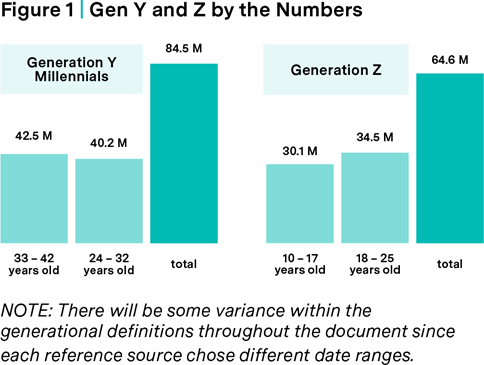

Millennials are the single largest living generation within the U.S. population. Their ranks bridge an 18-year span between the oldest (now 42) and the youngest (now 24). Beginning with its 2019 Home Buyers and Sellers Generational Report, the National Association of REALTORS began tracking the homebuying habits of the Millennial generation in two separate groups: Younger Gen

Y Millennials (born 1990 through 1998) and Older Gen Y Millennials (born in the years 1980 through 1989).

By the Numbers | Gen Y Millenials

- There are about 40 million Younger Gen Y Millennials (compared to 45 million Older Gen Y).7

- In 2022, the youngest Younger Gen Y Millennials will turn 24 and the oldest will turn 32.

How are Younger Millennials Different?

Younger Millennials are said to be more riskaverse compared to their older, experienceseeking counterparts. Experts say this is largely due to their age during two defining events: 9-11 and the Great Recession.

- Younger Millennials were too young to remember 9-11, a formative event that encouraged older Millennials to pursue their dreams instead of their careers.

- But Younger Millennials are old enough to remember how their Gen-X parents, older Millennials and others were affected by the economic downturn from the subprime mortgage crisis. This left a lasting impression on their outlooks and approaches to financial matters.

Today, Younger Gen Y Millennials are said to be attracted to industries with steady work. They’re less likely to job-hop and are more likely to say that they are willing to work overtime than older

Millennials.8

What else do we know about this cohort?

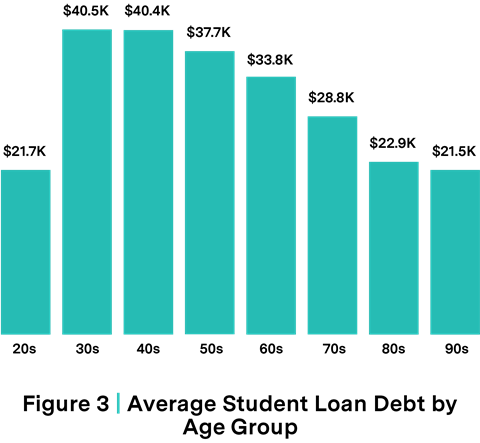

- Millennials in their 20s appear to be less burdened by student debt than Millennials in their 30s and 40s. Twenty somethings owe $21,700 on average. Thirty somethings owe almost twice as much ($40,500)9

- Young Millennial families have been more successful at building wealth compared to older Millennials at the same age.10

- Among non-homeowners, younger Millennials have better credit than older Millennials: Freddie Mac reports that 43% of younger Millennials who don’t have a mortgage could qualify for one. This compares to only 31% of older Millennials.11

- Younger Millennials are just beginning to flex their homebuying power.

Key Takeaway: Originators who lump younger Gen Y in with their older counterparts may be underestimating this cohort’s motivation and ability to buy.

Introducing Gen Z

Brookings Research defines Generation Z as those born in the years 1997 through 2012. In 2022, the oldest members of Gen Z will turn 25 and the youngest will turn 10. This generation is the most diverse of all cohorts and on track to becoming the best educated.

By the Numbers | Generation Z

- Approximately 34.5 million members of Generation Z are aged 18 and over.19

- Just over 7 million members of Generation Z are employed full time and they generate almost $229 billion in annual total income.14

- Members of Gen Z attending college are choosing majors that will yield practical, generously paying jobs.15

- By 2023, Gen Z will comprise 30% of the U.S. labor force.16

When it comes to finances, members of Gen Z are said to be motivated savers and careful spenders. Despite the Pandemic, 70% of the Generation Z members surveyed in 2021 added to their savings, 29% mapped out financial goals, 26% contributed to a retirement account, and 26% invested in the market.17 When they are considering a purchase, 96% of Generation Z said they read reviews or recommendations for products before buying.18 Many said they prioritize minimizing student debt or avoiding it altogether.19

What else do we know about this cohort?

- Nearly half of Gen Z members fall into the category of “minority.” 52% of Gen Z is white, 25% is Hispanic, 14% is Black and 4% is Asian.20

- Members of Gen Z are more likely to be first generation American: 22% of Gen Zers have at least one immigrant parent compared with 15% of all Millennials.21

- Compared to older generations, more members of Gen Z have at least one college-educated parent, they are less likely to drop out of high school, and more likely to earn a four-year

degree.22 - Advances in education are particularly notable for Hispanic and Black members of Gen Z. In 2017, 76% of Hispanic 18- to 20-year-olds had finished high school compared to only 60% in 2002. Among blacks, 77% aged 18 to 20 had finished high school compared with 71% in 2002.23

- Among all new homeowners in 2021, Latinos were twice as likely to have purchased a home at a young age: 34% were aged 18 to 24 compared to only 17% of the general population.24

Key Takeaway: Marketing to minorities will become even more important in the coming years as an increasingly educated cohort of Gen Z shifts the racial and ethnic balance of the homebuying public.

Defining Gen Y and Z

Definitions for Generations Y and Z are fluid. For example, Pew Research ends Gen Y at 1996 and begins Gen Z at 1997. The National Associationof REALTORS ends Gen Y at 1998 and begins

Gen Z at 1999. For the purposes of this white paper, unless otherwise noted:

- Gen Z is defined as those born in the years 1997 through 2012. In 2022, the oldest members of Gen Z will turn 25.

- Younger Gen Y Millennials are defined as those born in the years 1990 through 1998. In 2022, the youngest members of this cohort will turn 24 and the oldest will turn 32.

- Older Gen Y Millennials are defined as those born in the years 1980 through 1989. In 2022, the youngest members of this cohort will turn 33 and the oldest will turn 42.

Zillennials: The Tweener Generation

Loan officers and mortgage brokers who are active on social media may want to work the term Zillennial into their next post. A popular term on Tik Tok, Facebook and Twitter, Zillennials are the self-proclaimed “tweener” generation. They overlap the waning years of the Millennial generation and the beginning years of Generation Z. Zillennials share traits with both age groups.

Like Younger Gen Y Millennials, they experienced the transition from flip phone to smart phone, the switch from DVDs to streaming, and the impact of the 2008 recession. And like Gen Z, Zillennials are very connected to their smart phones and reliant on Wi-Fi. Zillennials tend to distinguish themselves from Gen Z and older Millennials by virtue of their pop culture references. They are proud of their in-between status as evidenced by websites such as bornzillennial.com.25

Younger Buyers Are Changing the Landscape of Home Buying.

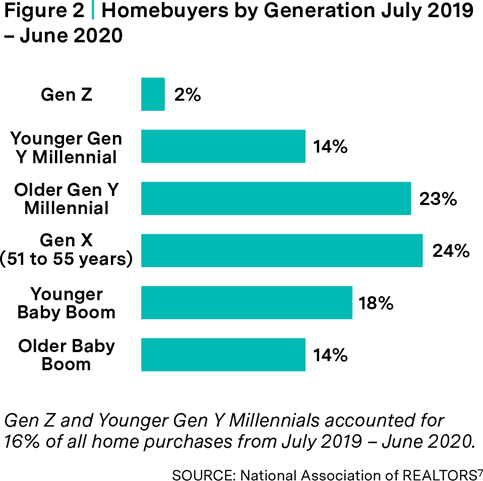

There’s a generational shift underway in the U.S. homebuying market. In 2020, Younger Gen Y Millennial homebuying grew faster than Older Generation Y, Gen X, and Baby Boomers. In another first, 2020 homebuyers included members of Generation Z, the nation’s newest generational cohort, born between 1997 and 2012.1

Buyer Profiles | Younger Gen Y Millennials

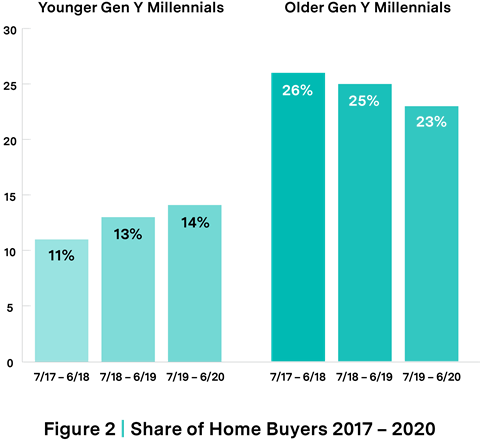

Like their older counterparts, Younger Gen Y Millennials have delayed milestones leading to household formation, but recent home sale trends indicate that is changing. Younger Gen Y Millennials accounted for 14% of all home sales from July 2019 to June 2020.2 This is a 27% increase from June 2017 to July 2018, when this demographic accounted for just 11% of home purchases.3

What do we know about Younger Gen Y homebuyers?

Following are results of a survey tracking generational differences among buyers who purchased homes between July 2019 through June 2020:

- The median homebuying age of Younger Gen Y Millennials was 27 years old (versus 35 years of age for Older Gen Y Millennials).

- Just over half (51%) were married (compared to 69% of Older Gen Y buyers), 20% were unmarried couples, 16% were single females and 11% were single males.

- Most Younger Gen Y buyers (73%) had no children (compared to 39% of Older Gen Y Millennials), 15% had one child, 8% had two, and 3% had three or more.

- 84% were White/Caucasian (compared to 80% of Older Gen Y Buyers), 9% were Hispanic/ Latino, 6% were Asian/Pacific Islander and 3% were Black/African-American.

- The median amount of student debt was lower for Younger Gen Y Millennials ($25,000) compared to Older Gen Y Millennials ($33,000) and the average for all buying cohorts ($30,000.).

- As expected, the vast majority (87%) were first- time home buyers.4

What did they buy?

- Young Gen Y Millennials tended to buy older, smaller, less expensive homes than Older Gen Y Millennials.

- Just over half of the homes purchased by Younger Gen Y Millennials were built between 1916 and 1984.

- Most had three bedrooms or more, but their median size was only 1,650 square feet compared to 2,000 square feet for Older Gen Y.

- Convenience to job, overall affordability of home, and convenience to friends and family were ranked high among their criteria for neighborhood choice.

- Younger Gen Y Millennials were also most likely to cite proximity to a veterinarian and outdoor space for a pet as a key consideration.

- 70% purchased homes for under $300,000 and their median home purchase price was $229,000.5

How did they pay for it?

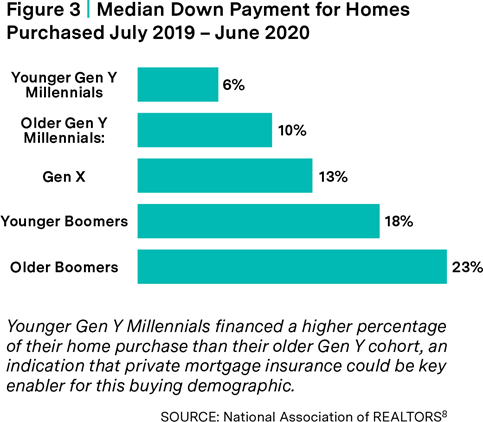

- Younger Gen Y Millennials made an average down payment of 6% -- the lowest of any age group.

- Only 13% of Younger Gen Y Millennials made a down payment of more than 20%.

- A substantial number (17%) made no down payment, more than any other age group.

- Among those who made a down payment, 84% drew from savings, 28% used a gift or a loan from a relative or a friend, 10% sold stocks or bonds and 10% used proceeds from the sale of a previous residence.

- Only 25% of Younger Gen Y Millennials said that saving for a down payment was the most difficult part of the homebuying process. Finding the right property (58%) ranked higher as did understanding the process and steps (33%).6

Key Takeaway: Younger Gen Y buyers struggled more with the homebuying process than they did with making the down payment, suggesting that originators who streamline mortgage search, selection and execution may have an edge.

|

|

Buyer Profile | Gen Z

The oldest members of Generation Z will turn 25 this year. As a percentage of the home- buying public, Gen Z are still in the low single digits; however, their participation in the market is expected to grow substantially as this demographic reaches peak home-buying ages. By some accounts, the market could see some 29 million potential buyers from Gen Z over the next five years.9

What do we know about Gen Z?

- Members of Gen Z as young as 18 through 21 are buying homes. In 2019/2020, this age group accounted for 2% of all homes purchased.10

- In Q2 2019, there were already 319,000 Gen Z with mortgages, a year-over-year increase of 112%.11

- Gen Z are building credit. In 2019, 14 million Gen Z had a credit card or another form of debt, up from 11 million the previous year. Another 13 million are expected to become credit eligible by 2Q 2022.13 A recent survey suggests many Gen Z will apply mainly to establish a credit score.14

- Gen Z are multi-taskers: In a 2018 survey focusing on Gen Z, nearly three quarters of respondents say they have a side job to help pay for their college education and expenses.15

- Gen Z are frugal: 26% percent of Gen Z college students surveyed in 2018 said they expect to graduate with no debt at all and an additional 26% expect to graduate with less than $25,000 in debt.16

- In yet another survey, 87% of Gen Z said they would like to own a home in the future, 68% said they consider homeownership as a way to build personal wealth, and nearly one third of older Gen Z said they had already started saving to buy a home.17, 18, 19

Key Takeaway: Gen Z are financially aware and expressing interest in homeownership. Originators who engage in financial literacy initiatives have an opportunity to tap into this interest and establish connections with this demographic before their homebuying process even begins.

Post COVID Sentiment

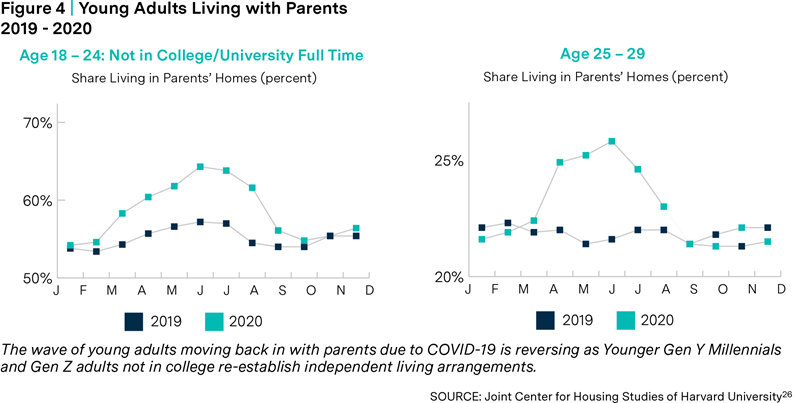

An estimated 450,000 Young Gen Y Millennials moved back in with their parents during the peak of the COVID-19 pandemic.20 By 2021, the vast majority had moved out again. In a survey of those who continued working during this time period, 83% said they were able to save money and 59% said those savings would go toward a down payment on a home.21

With the exception of college students, the vast majority of Gen Z who moved back home with parents during the pandemic have also moved out again.22 Despite financial and other pandemic-related challenges, a Gen Z survey of financial attitudes found that 68% of Gen Z remain optimistic about their financial future.23 Nearly 70% said the pandemic influenced their financial priorities, including a greater focus on saving for future goals (33%) and living a more frugal lifestyle (19%).24 Approximately 20 percent of Gen Z said they have become more eager to buy a home due to the coronavirus pandemic.25

Key Takeaway: Despite setbacks from COVID-19 and ongoing student debt, homeownership remains a top goal for both Younger Gen Y Millennials and Gen Z adults.

Are you ready for the generational shift in homebuying?

As noted in part one of this three- part series, Younger Gen Y homebuying grew significantly in 2019/2020 and as many as 29 million members of Gen Z could be shopping for homes by 2026.1 In Part Three, we discuss how loan originators can reach and resonate with this emerging home buyer demographic.

Digital Fluency

Younger Gen Y Millennials (born 1990 through 1998) can’t remember living in a world without technology.2 They grew up with the transition from dial-up to broadband, DVDs to streaming, and flip phones to smart phones.3 Ecommerce (think Amazon and Poshmark) and social media (think Snapchat and TikTok) are integral to their everyday lives.

Generation Z goes a step further. They enjoy the distinction of being the first generation of digital native, born into a world already awash in 24/7 internet access, WiFi mobility, online shopping, and viral memes. With technology literally at their fingertips, 70% of Gen Z would rather go without their wallet than their phone.4

For loan originators, a digital presence is almost essential for reaching these always-online generations. But getting noticed can be a challenge when we consider that reports suggest the average attention span of a Millennial is 12 seconds and the average attention span of Gen Z is only 8 seconds.5 As with marketing to any demographic group, a headline that captures the attention of one generation won’t necessarily be of interest to another. Within each demographic, it’s important to understand what topics do and don’t resonate.

What do we know about the interests of Younger Generation Y Millennials and Gen Z?

Money Talks. Younger generations are surprisingly savvy about the need for effective money management. Establishing credit history is a top priority for members of Gen Z while personal budgeting apps are especially popular with Millennials.6,7 When it comes to home financing, however, studies suggest that there’s an education gap. A 2019 Freddie Mac survey found that 39% of

younger Millennial respondents (ages 24 – 29) and 60% of Gen Z (ages 18-23) respondents were not confident in their knowledge of the overall homebuying process.8 An even greater percentage (45% of younger Millennials and 63% of Gen Z) of survey respondents were not confident in their knowledge of the types of mortgage loans available.9

In addition:

- 39% of Younger Millennials (ages 24 – 29) and 54% of Gen Z (ages 18-23) said they were not at all or not very confident in their knowledge of interest rates.10

- Among all Millennials, 42% said they weren’t sure or thought that home purchases required a minimum down payment of 20%.11

- Among Gen Z, more than one in four surveyed said they think they will need to put down more than 20% and more than 63% said they believe they will need to put down more than 11%.12

Key Takeaway: Loan originators have a unique opportunity to connect with Younger Gen Y and Gen Z through website blogs, social media posts, and videos that help to de-mystify

the various phases of the home buying and mortgage application process.

(Mobile) Technology Walks. The majority of Younger Gen Y and Gen Z aren’t ready to take the homebuying process entirely online.13 But that doesn’t mean these generations don’t love technology tools. For example:

- In a 2021 survey, younger generations were more likely to say they would be comfortable viewing a digital floor plan or 3D virtual tour, receiving email notifications from a real estate website or app, and unlocking a home with their phone and touring it on their own time.14

- Among those who bought a home in 2019/2020, 87% of Younger Gen Y homebuyers surveyed said they searched for homes on mobile or tablet devices.15

- A majority (86%) of younger homebuyers surveyed said they shopped for mortgages online (compared to only 55% of buyers aged 55+).16

Key Takeaway: If your company offers technology, flaunt it. Promoting mobile-friendly outreach, online applications, automatic updates, and eClosings can give loan originators an edge when it comes to winning business from Younger Gen Y Millennials and rising Gen Z.

It's Personal. Authenticity is a theme that resonates with Younger Gen Y and Gen Z perhaps due to their unprecedented degree of diversity. Younger Gen Y Millennials are more ethnically and culturally diverse compared to older generations. Gen Z is even more so: they are more likely to have been raised in a single parent household, an ethnically diverse household, or a household with non-traditional gender roles.17 Approximately one in six identify as LGBTQ and a third know someone who uses gender neutral pronouns.18, 19

According to surveys...

- Gen Z are 25% more likely than other generations to give up personal information in exchange for personalized recommendations.20

- 82% of Gen Z said they trust a company more when they use images of real customers in their advertising campaigns.21

- 43% of Gen Z-ers said they would participate in a product review and 62% of Gen Z said that good user reviews make them feel confident to buy.22

- When they are ready to purchase their first home, a significant majority of Gen Z (79%) said they would rather have face-to-face interactions with professionals than carry out the process fully online.23

Key Takeaway: Younger generations value authentic, personalized relationships with brands. Sharing personal stories – your own and those of your customers – is a great way for loan originators to connect and build relationships with Younger Gen Y Millennials and Gen Z.

Channeling Your Messages

Social media can be an effective channel for reaching Younger Gen Y Millennials and members of Gen Z. Both cohorts use social media regularly, but their channel preferences can vary. Facebook and YouTube, for example, are equally popular among Gen Z and Millennials, but the use of Instagram, Snapchat and TikTok are especially common among adults under 30.

Five Digital Content Starters

Whether you’re publishing a website blog, sharing an Instagram story, posting a tweet, or sending an email, content is often the biggest hurdle to overcome when reaching out to Younger Gen Y Millennials and Gen Z. Here are five content topic suggestions that can help get you started:

Highlight pet projects. Younger generations love their pets, so much so that in a recent survey more Millennials cited dogs over marriage or children as a key factor in their home purchasing decision.25 Loan originators can tap into this interest by showcasing photos and short stories about their own four-legged friends. Those without pets can still connect with younger generations by sharing information about local dog parks, pet-friendly restaurants, opportunities to donate to animal shelters and so forth.

Showcase renovation tips. Younger generations are shopping older, smaller, less expensive homes. Sharing links to before/after renovation photos, tips for vetting a responsible contractor, and profiles of older residential areas are just some ways in which loan originators can connect with first-time homebuyers in the Younger Gen Y and Gen Z age groups.

Demonstrate community involvement. Perhaps more than any other generation, societal issues are top of mind among Younger Gen Y Millennials and especially Gen Z. Let them know that

you care too by sharing your personal and/or corporate involvement in philanthropic efforts.

Demystify down payments. Studies continue to demonstrate a lack of awareness about down payment requirements among first-time homebuyers. A series of educational posts that demystify down payment requirements can establish loan originators as helpful advisors to Younger Gen Y and Gen Z.

Celebrate successes. Did you just help a young couple navigate the ins and outs of the mortgage application process? Close on the perfect home for a beloved pet? Feed into the appeal of authenticity among younger generations by putting a face on your successes. This could be as simple as asking for permission to post a photo of your most recent client.

DOWNLOAD PART 1 INFOGRAPHIC

DOWNLOAD PART 2 INFOGRAPHIC

DOWNLOAD PART 3 INFOGRAPHIC

References - Part 1:

1 https://www.roostify.com/resources/more-gen-zers-are-buyinghomes-than-ever-before

2 https://www.statista.com/statistics/1260224/share-of-gen-zprospective-home-buyers-usa/

3 https://www.realtor.com/research/gen-z-valueshomeownership/

4 2021-home-buyers-and-sellers-generational-trends-03-16-2021.pdf (nar.realtor)

5 https://www.brookings.edu/blog/the-avenue/2020/07/30/nowmore-than-half-of-americans-are-millennials-or-younger

6 2019-home-buyers-and-sellers-generational-trendsreport-08-16-2019.pdf (nar.realtor) | 2020-generational-trendsreport-03-05-2020.pdf (nar.realtor) | 2021-home-buyers-andsellers-generational-trends-03-16-2021.pdf (nar.realtor)

7 https://www.census.gov/newsroom/press-kits/2020/population-estimates-detailed.html -- Annual Estimates of the Resident Population by Single Year of Age and Sex: [for State] April 1, 2010 to July 1, 2019 | https://www.realtor.com/research/gen-z-values-homeownership/

8 https://www.thecut.com/2017/04/two-types-of-millennials.html

9 https://educationdata.org/student-loan-debt-by-age

10 https://www.newamerica.org/millennials/reports/emergingmillennial-wealth-gap/wealth-and-the-credit-health-of-youngmillennials/

11 https://marketsandmortgages.com/2021/12/14/millennialsdominate-housing-market/

12 https://educationdata.org/student-loan-debt-by-age

13 https://www.census.gov/newsroom/press-kits/2020/population-estimates-detailed.html -- Annual Estimates of the Resident Population by Single Year of Age and Sex: [for State] April 1, 2010 to July 1, 2019

14 https://www.nationalmortgagenews.com/list/6-importantthings-to-know-about-gen-zs-homeownership-goals

15 https://www.genzinsights.com/when-it-comes-to-money-weshould-all-act-more-like-gen-z

16 https://financesonline.com/generation-z-statistics/

17 Bank of America Better Money Habits Research Finds That, Despite Barriers, 80% of Gen Z Are Taking Positive Steps Toward Achieving their Financial Goals

18 8 Generation Z Trends & Predictions for 2022/2023: A Look Into What’s Next - Financesonline.com

19 https://www.genzinsights.com/when-it-comes-to-money-weshould-all-act-more-like-gen-z

20, 21, 22, 23 https://www.pewresearch.org/social-trends/2018/11/15/early-benchmarks-show-post-millennials-on-track-to-bemost-diverse-best-educated-generation-yet/

24 2021-state-of-hispanic-homeownership-report.pdf (nahrep.org)

25 https://www.urbandictionary.com/define.php?term=Zillennial

https://www.floridatoday.com/story/news/2021/05/04/zillennial-advocate-sparks-facebook-boom-promoting-his-1990-s-microgeneration/7182389002/

References - Part 2:

1,3 2019-home-buyers-and-sellers-generational-trends-report-08-16-2019.pdf (nar.realtor) | 2020-generational-trends- report-03-05-2020.pdf (nar.realtor) | 2021-home-buyers-and- sellers-generational-trends-03-16-2021.pdf (nar.realtor)

2 2021-home-buyers-and-sellers-generational-trends-03-16-2021. pdf (nar.realtor) | https://www1.roostify.com/the-resilience-of- the-american-homebuyer-during-covid-19-ebook (6.4 million new and existing home sales multiplied by .14)

4, 5, 6, 7, 8 2021-home-buyers-and-sellers-generational- trends-03-16-2021.pdf (nar.realtor)

9 https://www.nationalmortgagenews.com/news/nearly-29- million-gen-zers-could-be-trying-buy-a-home-by-2026

10 2021-home-buyers-and-sellers-generational-trends-03-16-2021. pdf (nar.realtor)

11 Forget waiting on Millennials, Gen Z is starting to buy homes - HousingWire

13 https://www.nationalmortgagenews.com/news/after-a-slow-start-low-rates-gen-z-could-sustain-mortgage-activity

14 https://www.genzinsights.com/when-it-comes-to-money-we- should-all-act-more-like-gen-z

15 https://www.genzinsights.com/when-it-comes-to-money-we- should-all-act-more-like-gen-z

16 https://www.genzinsights.com/when-it-comes-to-money-we- should-all-act-more-like-gen-z

17, 18 https://www.nationalmortgagenews.com/list/6-important- things-to-know-about-gen-zs-homeownership-goals

19 https://www.statista.com/topics/8404/gen-z-and-the-housing- market-in-the-us/#dossierKeyfigures

20 https://usafacts.org/data/topics/people-society/population- and-demographics/population-data/young-adults-living-at- home-25-34-yrs/

21 https://www.zillow.com/research/millennial-savings- homeownership-29709/

22 After a Brief Return, Young Adults Quick to Move Out of Parents Homes as the Pandemic Continues | Joint Center for Housing Studies (harvard.edu)

23, 24 https://newsroom.bankofamerica.com/content/newsroom/ press-releases/2021/10/bank-of-america-better-money- habits-research-finds-that--despite.html

25 https://www.statista.com/statistics/1220507/covid- homeownership-plans-genz-millennials-gen-x-baby-boomers- usa/

26 https://www.jchs.harvard.edu/blog/after-brief-return-young- adults-quick-move-out-parents-homes-pandemic-continues

27 https://www.lendingtree.com/home/mortgage/the-most- popular-us-cities-for-gen-z-homebuyers-ranked/

28 https://www.lendingtree.com/home/mortgage/most-popular- cities-millennial-homebuyers/

1 https://www.nationalmortgagenews.com/news/nearly-29- million-gen-zers-could-be-trying-buy-a-home-by-2026

2,3 https://www.cnn.com/2017/05/01/health/young-old-millennial- partner/index.html

4 https://www.kasasa.com/exchange/how-each-generation- handles-their-finances

5 https://later.com/blog/gen-z-vs-millennial/

6 When it comes to money, we should all take notes on these Gen Z habits (genzinsights.com)

7 https://www.cbinsights.com/research/report/millennials- industries-thriving/#finance

8,9, 10, 11 millennial-playbook.pdf (freddiemac.com)

12 https://press.homes.com/a-new-generation-of-homebuyers-is- here-meet-generation-z/#:~:text=Generation%20Z%20is%20 Highly%20Committed,homes%20at%20an%20earlier%20age

13, 14 https://www.zillow.com/research/digital-tools- millennials-29101/

15 2021-home-buyers-and-sellers-generational-trends-03-16-2021. pdf (nar.realtor)

16 https://www.forbes.com/sites/theyec/2021/06/01/how- millennials-are-changing-the-mortgage-and-home-buying- market/?sh=52c19a28690b

17 https://www.pewresearch.org/social-trends/2018/11/15/early- benchmarks-show-post-millennials-on-track-to-be-most- diverse-best-educated-generation-yet/

18 https://www.nytimes.com/2021/02/24/us/lgbt-identification- usa.html

19 https://www.pewresearch.org/social-trends/2020/05/14/on- the-cusp-of-adulthood-and-facing-an-uncertain-future-what- we-know-about-gen-z-so-far-2/

20 https://www.kasasa.com/exchange/how-each-generation- handles-their-finances

21 Cross-Generational Digital Marketing Insights For 2022 (forbes. com)

22 https://99firms.com/blog/generation-z-statistics/#gref

23 https://www.freddiemac.com/research/consumer- research/20191120-gen-z-ambitious-yet-realistic

24 https://www.pewresearch.org/internet/2021/04/07/social- media-use-in-2021/

25 https://www.thetruthaboutmortgage.com/millennials-are- buying-homes-to-give-their-dogs-room-to-roam/

Mortgage Insurance Premiums are Tax-Deductible: What it Means for Borrowers

Mortgage insurance (MI) premiums are once again tax-deductible, and this time, the benefit is here indefinitely. Learn more about what that means for borrowers and loan officers.

Navigating the Spring Market: Tips for Buying or Selling Your Home

Spring is the busiest season in real estate, with warmer weather and blooming flowers highlighting a property's best features, and buyers prioritizing home tours before family obligations. Take a look at our checklists to help buyers and sellers prepare for the upcoming busy market.

Why Buying a Home Still Makes Sense in Today's Market: A 2025 Perspective

In today's real estate landscape, potential homebuyers might hesitate to enter the market. However, despite current challenges, several compelling reasons make homeownership an attractive option. With proper planning and understanding of available options, buying a home in 2025 can be a smart investment in your future.

Beyond the Rate Drop: Helping to Future-Proof Your Lending Strategy

The recent drop in interest rates may lead to an influx of purchase and refi volume for lenders. With this shift on the horizon, learn more about positioning yourself to meet customer needs and help borrowers at scale through proper use of technology and innovative solutions.

Homebuying Trends in the United States

Discover the state of homeownership in the US, including the significant disparities across racial and ethnic lines and the challenges that homebuyers face. Learn about the importance of addressing these disparities and creating more equitable pathways to homeownership for building wealth and ensuring accessibility for all.

Debunking 7 Common Mortgage Myths

The homebuying process can be exciting, but it can also be overwhelming, especially when it comes to mortgages. There's a lot of information out there, but not all of it is accurate. In this article, we debunk some common mortgage and PMI myths to help borrowers make better informed financial decisions.

Explore the Evolving Traits of First-Time Homebuyers

Our infographic explores the characteristics and behaviors of today's first-time homebuyers, who prioritize homeownership as an important part of the American Dream despite economic and societal changes.

Loan Officers' Social Media Checklist: Best Practices to Help Build Your Brand

Loan officers can benefit from social media to connect with potential borrowers, build their brand, and establish themselves as a reliable authority in the mortgage industry. Optimizing social media profiles and posting strategies can attract new business and create lasting relationships with borrowers and business professionals. Check out our checklists to get started!

The American Dream of Homeownership Starts with Financial Literacy

As we celebrate National Financial Literacy month this April, it’s a reminder of the important role that financial literacy plays in preparing for the homebuying journey. Learn more about financial literacy for homebuyers.

4 Simple Steps for Loan Officers to Build Lasting Relationships in 2024

Using these 4 Simple Steps, Loan Officers can help their elevate business and redefine success in 2024 by building strong relationships with real estate agents, prior clients, local community organizations, and other trusted service providers.